How Much Do You Need To Retire? Find out with this Retirement Calculator

Takeaways

- Determine your current financial trajectory using this Retirement Calculator

- Don't freak out: Your Retirement Calculator results may indicate that 10 to 15 years from now, you're making about the same amount of money, paying more taxes, and noticing it is harder to cover your cost of living, let alone save for retirement.

Action Items

- Get curious by updating the spreadsheet to see the impact of your income, retirement savings, and where you decide to live.

- Reflect on Values and Desires: Take time to evaluate personal values and passions to curate a retirement plan that aligns with individual aspirations.

- Create a Retirement Vision Board: Envision the ideal retired life by creating a vision board with images and words representing desired goals and lifestyle, serving as a guiding reminder throughout the financial planning journey.

Disclaimer: The projected values below are based on estimates. We recommend conducting comprehensive research to develop a retirement plan tailored to your individual needs and circumstances. The spreadsheet serves as a tool to help you consider future planning and initiate continuous learning about your retirement.

Planning for retirement can get complicated. We either are not thinking about it cause it's so far away or often think we've got it all figured out, but then reality hits. The things we are told (put money away in your 401K for retirement!) don't always match our actual situation or ability to save. It's important to understand the factors that impact our retirement savings because expenses have a way of piling up unexpectedly. To really grasp your retirement plan, analyze your finances and see how they'll change over time. Look at healthcare costs, taxes, and how your salary is split into these different buckets, especially over time.

We created a

retirement calculator

to help illustrate the importance of understanding how your money grows (or doesn't) over time. We recommend opening this sheet with us and inputting the numbers as we go. Let's dive in!

Understanding the Retirement Calculator

At first glance, this may appear daunting, but let's focus on the first column for now. Input or select only the options highlighted in the yellow cells. All other cells will auto-populate based on your responses.

However, if you have a good understanding of your market and want to update certain sections, such as State Tax, which has been estimated, feel free to input your own figures. I recommend making changes at the end once you have a clearer picture.

Our Step-by-Step Guide on How to use this retirement calculator (for visual learners, scroll down to see an animated instructions below):

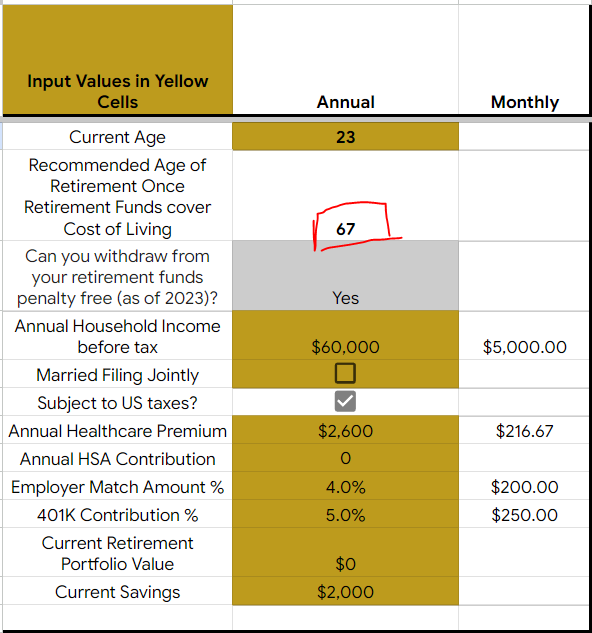

- Current Age: Enter your current age. For example, if you were born in 2002, you would input 21.

- In our example, we are 23 years old.

- Annual Household Income Before Tax: Input your gross salary figure, the amount you were offered upon hire. For instance, if you were offered a salary of $60,000 or $25.50 per hour, multiply $25.50 by the number of hours you anticipate working in a year (typically 1,880 hours after accounting for holidays, vacation, and sick time based on American standards).

- In our example, we used $60,000.

- Married Filing Jointly: Check this box if you are married and plan to file your taxes jointly.

- In our example, we are not married so left it blank.

- Annual Healthcare Premium: Enter your annual healthcare cost. Check your paystub to see how much you pay monthly or bi-weekly, and multiply it by 12 if you are paid monthly, 24 if paid twice a month, or 26 if paid every two weeks.

- In our example, the healthcare cost is $100 every two weeks, resulting in $2,600 annually.

- Annual HSA Contribution: If you have a high deductible plan, you likely have the option to contribute to a Health Savings Account (HSA) at work. This account allows you to invest money that grows tax-free, but can only be used for healthcare expenses.

- In our example, we do not contribute to our HSA ($0).

- 401K Match Amount: This is the amount your employer contributes to your 401K account. Typically expressed as a percentage of your salary, it often requires you to contribute a certain percentage of your income to receive the employer match. The percentage may vary by employer.

- In our example, the employer contributes 100% of the first 4% and 50% of the next 2% of our contribution. To receive the full 4% match, we would need to contribute 5% of our salary. Therefore, we entered in a 4% match amount from the employer.

- 401K Contribution %: Input the percentage you contribute to your 401K on a yearly basis.

- In our example, we contribute 5% to receive the full employer match of 4%.

- Current Retirement Portfolio Value: Enter the total value of your current retirement portfolio, including all values in your IRA and other 401K accounts you may have accumulated over time.

- In our example, we entered $0 since this is our first job and we haven't started saving for retirement yet.

- Current Savings: Input your total savings minus any debt. You may also consider including other debt items like student loans, car payments, or a mortgage to get a better understanding of your financial situation.

- In our example, we'll say after debt, we have no money in savings.

- Cost of Living: Here you should select one of the following options:

- Select one of the provided options based on the average cost of living for a single person with no children living in a one-bedroom apartment in 2023.This will automatically populate based on data available by Numbeo, Department of Housing and Urban Development (HUD), and Economic Policy Institute (EPI).

- Alternatively, you can use the custom parameters to input your own data. You must check the box custom.

- If you own a house, check this box and input your Home Value and Years left on your mortgage payment.

- The spreadsheet will also guestimate an “Expected Annual Rate of House Upkeep (expressed as a percentage of the Home Value). We have kept this amount to a conservative annual maintenance to be 2% of your home equity value on average for the life of your mortgage.

- If you do not own a house, you can skip these questions and go straight to Monthly rent/mortgage. Input your rent costs and your estimated monthly cost of living. If you’re unsure, you can check out our suggestions in major cities to determine your estimated monthly expense.

- In our example, we rent in Philadelphia and use the data provided for us by the Economic Policy Institute (EPI).

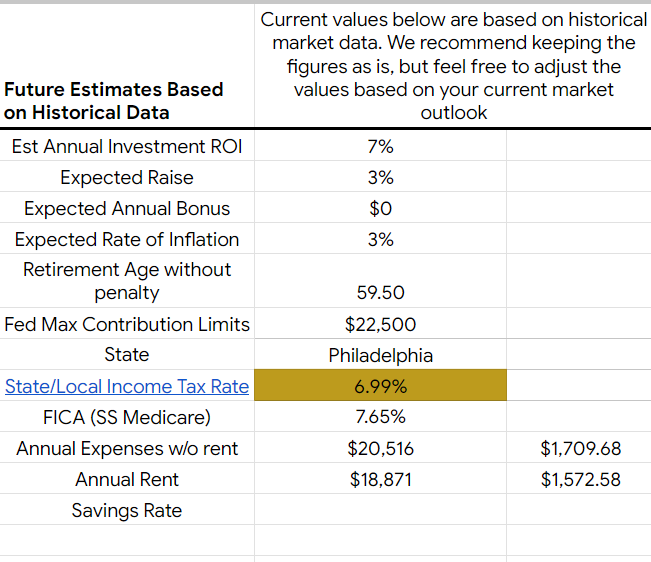

In this section, "Future Estimates Based on Historical Data", seen above, we see what estimates are used to calculate the data in the worksheet. You don’t need to update these numbers, but if you’d like to play around, feel free to toggle the numbers to see how it affects your overall financial outcome. Note that the input for "State/Local Income Tax Rate" is a broad estimate. If you'd like a better analysis of your potential state/local income tax rate, click the link in the spreadsheet and input your estimated income. You can update this box to reflect a more accurate percentage based on your circumstance.

- In our example, we left it as it is.

Analyzing the Numbers

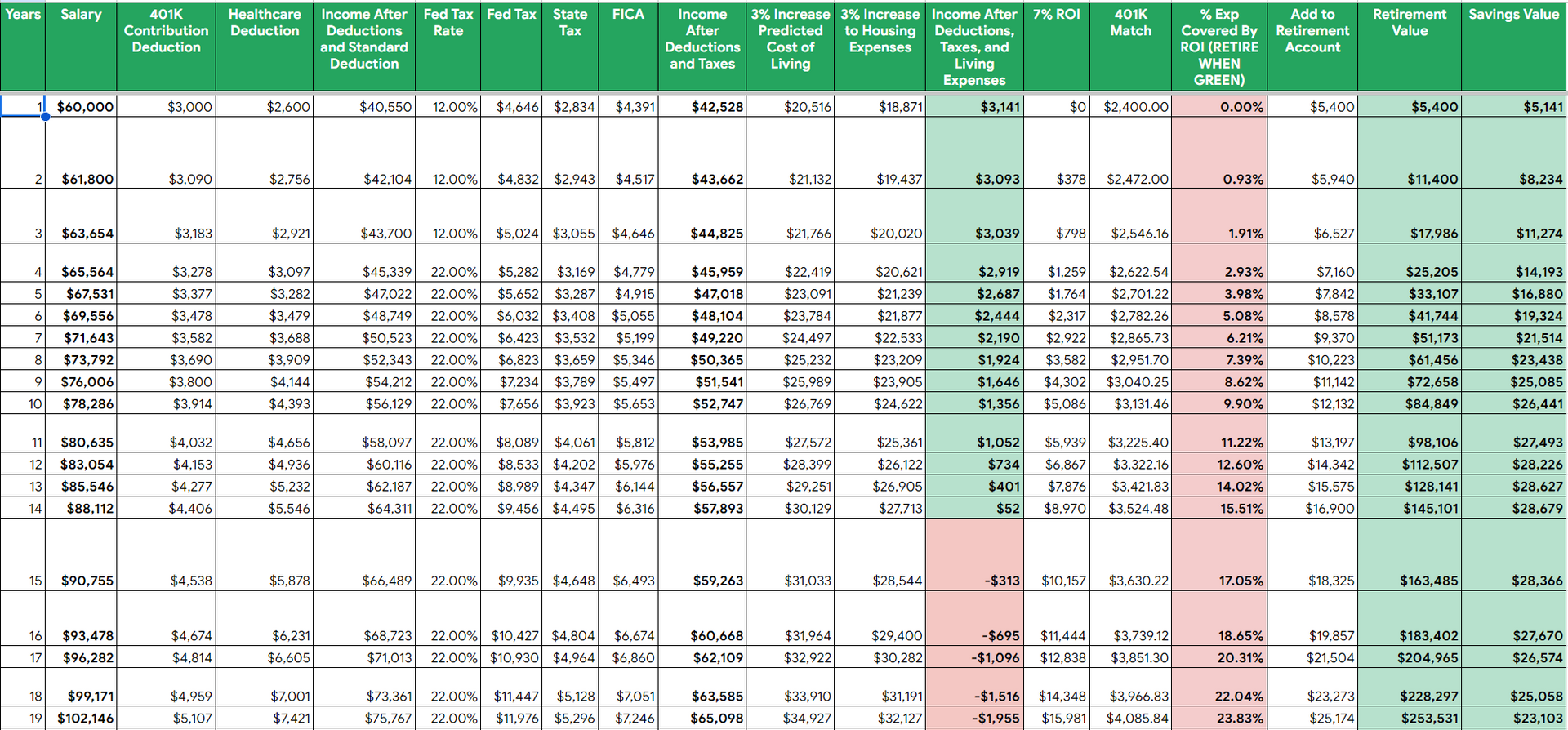

In our example, at 23 years old with an annual salary of $60,000. We have a modest healthcare plan costing $200 per month, and we're contributing 5% to our 401K to receive the full employer match of 4%, resulting in a $5,400 contribution towards retirement. We don't have any debt and $2,000 in savings. Rent in Philadelphia amounts to $1,572.58 per month for a one-bedroom apartment, while the cost of living (food, transportation, utilities) is estimated at $1,709.68 per month for one person.

Upon examining the Retirement Calculator and basic retirement standards, it appears that we're doing fairly well. By consistently contributing 5% towards our retirement savings, we are projected to retire comfortably at the age of 67. At that point, we can start withdrawing from our retirement accounts and rely on the earnings they generate, without depleting the principal amount we initially invested.

However, things start to get challenging when we turn 38 years old and around 15 years into our career. Here, our income is negative after deductions, taxes, and living expenses. Suddenly, it becomes harder to cover our cost of living, let alone save for retirement. What's causing this affordability issue? Well, it's a combination of our cost of living and rent gradually increasing by 3% due to inflation. On top of that, our taxes have risen from 12% to 22% since we started. Although our salary has risen to $90,000, or 50% more when we made $60,000, our cost of living has also stayed on pace with our salary increase. We are effectively making the same amount we did 15 years ago, but paying more taxes. It's clear that we'll need to make some adjustments. We can either reduce our retirement savings, cut down on expenses, find ways to increase our income, or consider the possibility of moving to a more affordable location.

What to do next?

Don't freak out. This incredible step of understanding your finances and retirement needs is a huge one. Leverage these learnings to get more curious and play an active role in your financial decisions and success planning. As we age and decide to get married or not, have kids or not, it becomes increasingly vital to adapt our financial strategies to secure options for yourself and your tribe. This may involve exploring opportunities to boost our income, identifying areas where expenses can be reduced, considering the possibility of relocating to more affordable regions, and making necessary adjustments to our retirement savings. Understanding the retirement strategy that aligns with your unique goals, circumstances, preferences, and dreams is essential. Come back to this Retirement Calculator and replug in numbers as you consider and accept new jobs, explore cities you want to move to, and get comfortable seeing a holistic picture of your finances overtime. Ignorance is not bliss when it comes to setting our future self up for financial security.

Disclaimer: The provided spreadsheet is intended for informational purposes only and should not be solely relied upon for financial planning. It is an estimate based on projected and estimated variables and may not accurately reflect your specific financial situation. It is essential to consult with a qualified financial advisor or conduct comprehensive research to develop a comprehensive retirement plan tailored to your individual needs and circumstances. The spreadsheet serves as a tool to help you consider future planning and initiate discussions about your eventual retirement.

How it works